Tariffs

INVESTMENT COMMITTEE COMMENTARY January 2025

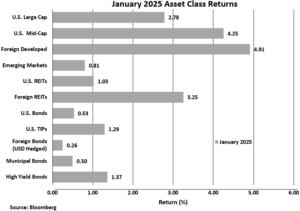

Equities opened the year higher as market optimism carried into 2025. For context, the S&P 500 just finished the best two-year performance period since 1997-1998 with a total return of greater than 25% for each of the last two years. While positive investor sentiment continues, another strong year for the S&P 500 would be an infrequent occurrence. Since 1928, there have been only five stretches with three consecutive 10%-plus returns and only once has there been a stretch of five consecutive 20%-plus returns (1995-1999). Of note, the equity markets exhibited broader depth in January as U.S. mid-cap, U.S. small-cap and foreign developed stocks outpaced the S&P 500.

The S&P 500 gained 3.3% in January. U.S. mid-cap and small-cap stocks rose 5.1% and 3.5%, respectively, while foreign developed stocks were up 5.3%. The S&P 500 was impacted by a sharp pullback in Nvidia Corp. (NVDA) shares which fell by 17% ($590 billion of market cap) on January 27th. Nvidia has led U.S. equities higher over the last two years, but innovations by Chinese company DeepSeek in its approach to artificial intelligence (AI) caused investors to take pause. DeepSeek may be a lower cost AI alternative and investors are evaluating the high valuations of chip developer Nvidia in light of the new technology competition.

Bonds had positive January performance. The yield on 10-year Treasury bonds remained flat from the prior month at 4.58% but hit an intra-month high of 4.79%. As expected, the Federal Open Market Committee (Fed) maintained the federal funds rate at the current 4.25%-4.50% following its meeting in January. In arriving at its decision, the Committee noted that the economy continued to expand at a solid pace and the labor market remained solid. Inflation, while it had eased, remained somewhat elevated. As to future policy actions, the Fed stated that “the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks.” The Bloomberg U.S. Aggregate Bond Index rose by 0.7% for the month. Other bond sub-indexes were also positive in January. Of note, U.S. Treasury Inflation-Protected Securities (TIPS) and high yield bonds had January total returns of 1.2% and 1.4%, respectively.

Tariffs

News on trade and tariffs has been accelerating and sometimes dramatically changing on a day-by-day basis. It is important for investors to distinguish between market noise and actual implementation.

A tariff is a duty or tax paid on goods imported into the country imposing the tariff. There are various reasons that a government may impose tariffs on goods produced in foreign countries. For example, a tariff brings revenue to the government imposing the tariff, and it may protect a strategic industry. The cost of the tariff is either absorbed by the company importing the goods or passed along to end consumers.

In the context of the second Trump Administration, the primary objectives of the tariffs appear to be less about tariff revenue and more about advancing a broader policy agenda. A key Trump issue is protecting and promoting U.S. companies and products from foreign competitors. Also, Trump seeks to have foreign countries come alongside the U.S. in objectives related to immigration, drug trafficking, trade deficits (balance of trade) and influences from China.

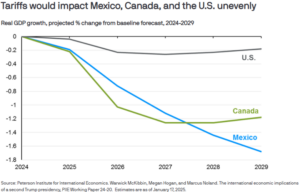

Tariff consequences may include inflationary pressures in specific industries or products, economic stagnation or declines in real gross domestic product (GDP) growth, and impacts on countries who have traditionally been significant trading partners with the U.S. The following chart from J.P. Morgan Asset Management illustrates the potential uneven impact of proposed tariffs between the U.S., Mexico and Canada.

The scale, scope and impact of Trump imposed or proposed tariffs is difficult to forecast. Tariffs impact markets, specific industries and countries in different ways. There are many potential outcomes, and so uncertainty is higher until policies are better defined and specified.

Until recently, the markets viewed tariffs more as a short-term negotiating tool of President Trump rather than a long-term real risk. For example, Trump issued a tariff threat to Colombia which did not come to fruition. The announced 25% tariffs to Canada and Mexico are now delayed for 30 days and some believe that heavy tariffs on key trading partners will not be implemented. Evidence suggests, however, that negative risks of tariffs on markets have risen.

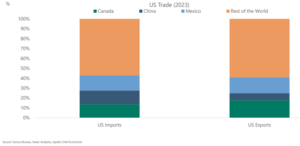

The U.S. is the world’s largest economy with cumulative gross domestic product of $29 trillion compared to China as the second largest economy of $18 trillion followed by Japan’s economy of $4 trillion. The following chart from Apollo Global Management highlights larger U.S. trading partners. The U.S. is the world’s biggest customer, and the trade policies of the Trump Administration are exerting economic power to advance the U.S. agenda.

Canada, China and Mexico make up 43% of U.S. imports and 40% of U.S. exports.

Data gives some indication of where real tariff risks may come from once “trade threats” are advanced.

- Tariffs are a bigger problem for U.S. trade partners than the U.S. due to the size and strength of the U.S. economy. The one exception is China which exports a lower percentage of its GDP (about 3%) to the U.S. Further, since 2000, China has become the main trade partner to most countries around the world including much of Asia, Africa and South America. China has a positive trade balance and strong economic influence globally.

- For China, tariffs will have a greater impact on consumer electronics such as smart phones, portable computers, lithium batteries and game consoles.

- For Canada, oil and gas and transport equipment (cars and trucks) will be more impacted by tariffs.

- For Mexico, transport equipment will also be impacted.

As a final note, U.S. exporters are not immune from trade policy risks. If countries set retaliatory tariffs, specific industries can be significantly affected. For example, exporters of aircraft and aircraft parts deal in high dollar goods and would be hurt by an extended trade war. Other industries and products might be less impacted by tariffs as consumer demand could remain stable with manageable economic consequences.

Concluding Comments

The U.S. economy appears strong, with steady growth and stable inflation. The Federal Reserve is on hold due to imbalances in labor markets and potential tax cuts. Changing trade policy and tariffs have created uncertainty, and the situation is fluid. There will likely be winners and losers as trade policies change. The U.S. can benefit if its balance of trade improves. This is what Trump has in mind as he discusses tariff reciprocity.

From an investing standpoint, broad diversification remains important and use caution in holding concentrated and high valuation stocks which have greater downside risk if negative news surprises investors.

If you have any questions, please consult your JMG Advisor.

Important Disclosure

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by JMG Financial Group Ltd. (“JMG”), or any non-investment related content, made reference to directly or indirectly in this writing will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this writing serves as the receipt of, or as a substitute for, personalized investment advice from JMG. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. JMG is neither a law firm, nor a certified public accounting firm, and no portion of the content provided in this writing should be construed as legal or accounting advice. A copy of JMG’s current written disclosure Brochure discussing our advisory services and fees is available upon request. If you are a JMG client, please remember to contact JMG, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. JMG shall continue to rely on the accuracy of information that you have provided.

To the extent provided in this writing, historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices. Indices are not available for direct investment.

Market Segment (index representation) as follows: U.S. Large Cap (S&P Total Return); U.S. Mid-Cap (Russell Midcap Index Total Return); Foreign Developed (FTSE Developed Ex U.S. NR USD); Emerging Markets (FTSE Emerging NR USD); U.S. REITs (FTSE NAREIT Equity Total Return Index); Foreign REITs (FTSE EPRA/NAREIT Developed Real Estate Ex U.S. TR); U.S Bonds (Bloomberg US Aggregate Bond Index); U.S. TIPs (Bloomberg US Treasury Inflation-Linked Bond Index); Foreign Bond (USD Hedged) (Bloomberg Global Aggregate Ex US TR Hedged); Municipal Bonds (Bloomberg US Municipal Bond Index); High Yield Bonds (Bloomberg US Corporate High Yield Index).