Tariff Announcements

With the recent market volatility and economic uncertainty following the tariff announcements, we first want to address these recent events before providing the March 2025 market review.

Tariff Announcements

Stocks begin the second quarter of 2025 following the worst quarterly performance in nearly three years. After President Trump’s tariff announcements on April 2nd of a substantial increase in tariffs that will be applied to goods imported from America’s global trading partners, equity markets across the globe fell further. Although history has recorded numerous stock market corrections, many investors have never experienced anything like the recent deep and rapid decline in the equity markets. Driving investor uncertainty, financial news is focused on the tariffs and the immediate reactions of the markets. As the speculations regarding each country’s retaliatory measures are still widely unknown, we will continue to monitor.

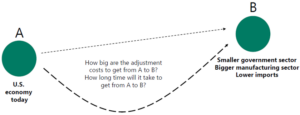

In addition to the impact of the tariffs on the markets, it seems that current policy goals of a smaller U.S. government, more U.S. manufacturing, reliable domestic supply chains, and lower imports leading to reduced U.S. trade deficits will likely have a near-term negative impact on GDP growth and corporate earnings. A longer implementation timeline will also add to near-term market volatility.

The following illustration is by Apollo Chief Economist, Torsten Slok, and shows adjustments are required to move toward the above stated objectives.

While the policies and implementation can be challenged and debated, the efficacy of the policies will determine if the desired goals are achieved. It is too early to know the final outcomes. The breadth and scope of the adjustments has been a surprise to the markets and has resulted in market volatility, a decline in stock prices, a decline in 10-year Treasury yields, and a decline in the value of the dollar.

Measures to Navigate This Difficult Market Period

Fortunately, JMG client portfolios are diversified between stocks and bonds. Diversification can be powerful during periods of stock market and economic uncertainty to help investors mitigate losses. In the current environment, bond valuations are holding up as expected and while bonds do not fully hedge the equity market declines, bonds generally have positive year-to-date returns.

Defined asset allocation strategies serve as a blueprint for generally proper actions in market decline environments. Assuming that an investor’s personal situation and financial goals are unchanged, the strategy is to rebalance back to the predefined allocation targets in stock market corrections. This strategy entails selling securities that have done much better and buying securities that have suffered price declines. This approach relies on the historical basis that markets eventually turn higher as companies adapt and figure out how to profitably navigate in the circumstances.

For some individuals, steep market declines are so uncomfortable that the inclination is to sell risk assets and move to cash. The desire to step out of stocks until “things settle down” is very normal in uncertain markets. However, tactical moves to cash are often unsuccessful because market timing is extremely difficult and more often leads to permanent losses of capital.

We understand that declining markets are often difficult to endure and the following are points to keep in mind.

- While markets are clearly facing legitimate headwinds, it is important to realize that stocks fell in the first quarter mostly on fears of what might happen in the economy and not because of what occurred. If future policy decisions and an economic slowdown are not as bad as currently feared, it could lead to a substantial market rebound in the coming months.

- While fears of a slowdown surged in the first quarter, economic data stayed mostly resilient. Jobless claims remained subdued, measures of manufacturing and service activity showed continued expansion, and the unemployment rate remained historically low, near 4.0%. Put simply, there was little in the actual data in the first quarter to imply the economy is weakening. If economic data remains stable throughout the second quarter, it will push back recession fears and could help fuel a rebound in the markets.

- On market valuation, the recent stock market declines have resulted in the S&P 500 trading at a more reasonable valuation compared to the start of the year. Extremely bullish investor sentiment has been replaced by a decidedly bearish outlook (which has historically set the stage for a market rebound).

- While U.S. stocks have declined this year, foreign stocks and bonds have held up well.

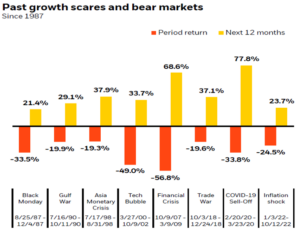

Finally, JMG’s advisor group has successfully navigated our clients through extremely difficult periods in our 40-year history, including the dot-com market crash of 2000-2002, the great financial crisis of 2007-2009, the COVID sell-off in 2020, and the inflation-fueled bear market in 2022. We are confident in our ability to help clients navigate through this and future market challenges to achieve their long-term goals and objectives.

If you have any questions or concerns, your JMG Advisor is standing by to help.

INVESTMENT COMMITTEE COMMENTARY March 2025

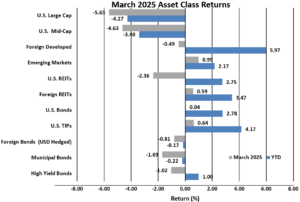

U.S. equity indexes generally fell in March. The market volatility that began in February increased in March. Tariffs, renewed inflation fears, and the threat of global economic stagnation worried investors. Consumer confidence fell to a 12-year low as uncertain U.S. trade and tariff policies raised concerns that economic and corporate earnings growth would dramatically slow or disappoint.

The S&P 500 declined by 5.6% in March. Declines in equities accelerated as President Trump made good on his warning to implement 25% tariffs on Mexico and Canada (and an additional 10% tariff on China). President Trump delayed some of those tariffs on Mexico and Canada until early April, but many other tariffs were left in place and that shattered investors’ belief that tariffs were just a negotiating tactic. Meanwhile, several corporations in various sectors began to report lower earnings guidance citing reduced consumer spending and business investment. Those guidance cuts reinforced fears that policy uncertainty could cause an economic slowdown, and the S&P 500 fell to a six-month low. In late March, markets tried to rebound amidst a lull in tariff news, but it did not last as President Trump announced 25% auto tariffs on March 26th, sending stocks lower once again. The S&P 500 finished the quarter near year-to-date lows.

In summary, investor optimism for a Trump Administration pro-growth and tax cuts agenda was replaced by rising concerns about a new global trade war and a slowing U.S. economy. Policy uncertainty and ineffective communication negatively impacted investor and consumer confidence.

In the bond markets, the yield on 10-year Treasury bonds was roughly unchanged in March at 4.23% and the Bloomberg U.S. Aggregate Bond Index had a flat return. The Federal Reserve kept rates steady at its March meeting. For corporate bonds, high yield bonds lagged higher quality investment grade bonds, again reflecting investor concerns about future economic growth and increased likelihood of recession.

![]()

Important Disclosure

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by JMG Financial Group Ltd. (“JMG”), or any non-investment related content, made reference to directly or indirectly in this writing will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this writing serves as the receipt of, or as a substitute for, personalized investment advice from JMG. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. JMG is neither a law firm, nor a certified public accounting firm, and no portion of the content provided in this writing should be construed as legal or accounting advice. A copy of JMG’s current written disclosure Brochure discussing our advisory services and fees is available upon request. If you are a JMG client, please remember to contact JMG, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. JMG shall continue to rely on the accuracy of information that you have provided.

To the extent provided in this writing, historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices. Indices are not available for direct investment.

Market Segment (index representation) as follows: U.S. Large Cap (S&P Total Return); U.S. Mid-Cap (Russell Midcap Index Total Return); Foreign Developed (FTSE Developed Ex U.S. NR USD); Emerging Markets (FTSE Emerging NR USD); U.S. REITs (FTSE NAREIT Equity Total Return Index); Foreign REITs (FTSE EPRA/NAREIT Developed Real Estate Ex U.S. TR); U.S Bonds (Bloomberg US Aggregate Bond Index); U.S. TIPs (Bloomberg US Treasury Inflation-Linked Bond Index); Foreign Bond (USD Hedged) (Bloomberg Global Aggregate Ex US TR Hedged); Municipal Bonds (Bloomberg US Municipal Bond Index); High Yield Bonds (Bloomberg US Corporate High Yield Index).