Post-U.S. Elections Takeaways and Implications

INVESTMENT COMMITTEE COMMENTARY November 2024

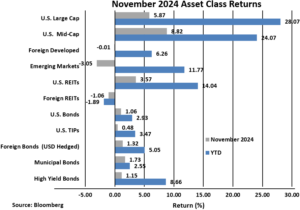

The S&P 500 had its best month of the year, rising 5.9%. The gains reflected investor optimism that a second Trump administration will favor businesses, but with the hope that the President-elect will take a more moderate stance on trade tariffs. All eleven market sectors ended November higher, led by consumer discretionary and financials.

While the S&P 500 had strong gains, U.S. mid-cap and small-cap stocks performed even better and rose 8.8% and 11.0%, respectively. International stocks were less favored by investors. Foreign developed country stocks were flat in November. Emerging market stocks fell by 3.1%. U.S. real estate investment trusts (REITs) rose 3.6% for the month.

On November 7th, the Federal Reserve (Fed) cut the Fed funds rate another 0.25%, meeting market expectations. Fed rate cuts and the expectation for future rate cuts have been important in supporting the recent stock rally. The election does not appear to have changed investors’ views of the Fed remaining in a rate cutting cycle.

However, as we discussed last month, recent interest rate movements have been unusual. Since the Fed’s initial 0.50% rate cut in September, the 10-year Treasury yield has risen sharply. Therefore, the inverted yield curve (where short-term interest rates are higher than long-term interest rates) seems to be moving closer to normal. This is important for two reasons. The “soft landing” that investors are hoping for cannot happen until the yield curve normalizes, but without a recession. Yet, if long-term rates move too high, this would not be favorable to economic growth, increase the chance of recession and be a headwind to the stock market. Expect market volatility due to this uncertainty.

Impacted by pro-growth economic hopes with controlled inflation, bond prices in November rose early in the month as the yield on 10-year Treasuries increased from 4.28% to 4.44% before falling to 4.18%. The Bloomberg U.S. Aggregate Bond Index (AGG) posted a 1.1% return for the month. Other bond sub-indexes also rose for the month.

Post-U.S. Elections Takeaways and Implications

In November, former President Trump won both the electoral college vote and the popular vote. He will lead the United States for a second, non-consecutive presidential term. Regarding Congressional elections, Republicans flipped the U.S. Senate and will hold a 53 to 47 seat majority. In the U.S. House of Representatives, Republicans held on for a razor thin 220 to 215 seat majority.

While majorities matter, the margins of the majority also matter. The narrowness of the Republican majorities in Congress will make Trump administration initiatives harder to pass. This could include additional tax cuts (no tax on tips, no tax on social security) and possible spending cuts that might be proposed by Elon Musk and Vivek Ramaswamy through the Department of Government Efficiency (DOGE). Also, the existing Tax Cuts and Jobs Act (TCJA) is scheduled to expire on December 31, 2025. While there is a greater chance TCJA will now be extended, at least in part, extension must go through Congress and not by executive action. This is not a binary decision as individual tax rates, the $10,000 state and local tax (SALT) deduction, personal exemptions, child tax credits, business and estate tax provisions (and more) are potentially impacted. Because of the dynamics in Congress, it is too early to tell how the issues will be resolved. Developments will need to be monitored in 2025 and financial planning must be prepared for multiple outcomes.

President-elect Trump has broad discretion to unilaterally act in certain areas on inauguration day, including tariffs, executive orders, and regulatory priorities.

Tariffs

While tax and spending policies must go through Congress per the Constitution, Congress has given power over tariffs to the executive branch through the 1974 Trade Act (fast track authority). Therefore, Trump can most likely act quickly on tariffs.

Not all tariffs are created equally. Small increases may be able to go through more easily. For example, there could be a further increase of tariffs on a list of Chinese products rather than a blanket tariff. However, Trump has also threatened other tariffs of 25% or 100% on Mexico, Canada, Brazil, Russia, and India. Such large tariffs would require Trump to declare a “national emergency” which potentially could be delayed by litigation.

Executive Orders

Trump is expected to roll-back executive orders issued by President Biden. For example, Trump appears likely to reverse or modify orders pausing new authorizations for the export of liquid natural gas and prohibitions of drilling on public lands. He is also likely to reverse or modify immigration enforcement and funding for sanctuary states. Numerous executive actions, beyond the scope of this writing, related to foreign affairs policies, reshaping the federal government, and changing/reversing social and education policies, all appear on the table.

Regulatory Enforcement

As the chief executive, through his appointed department heads, Trump also has authority to direct the regulatory priorities of the federal government. In areas ranging from the financial system to the environment to food safety and border security, the federal government may change the level or focus of regulatory enforcement.

Impacts

Some are worried that tariffs or “mass deportations” will fuel a new wave of inflation, or meaningfully reduce growth, or both. While we recognize these arguments, we think that taken as a whole, the impact of Trump’s policies is not yet clear. There will be offsetting effects of his various policies, and the degree to which they are implemented (due to legal, political, or diplomatic factors) is also unclear. It is essential to remember that the economy is not solely controlled by government policy.

Externalities

The U.S. federal deficit is running above $2 trillion. The U.S. national debt is above $36 trillion (130% of GDP) and growing. By reference, total annual federal tax revenue is about $5 trillion of which tariff tax revenue is about $70 billion. (Source: usdebtclock.org). These levels will eventually need to be addressed. At the same time, the US economy appears to be on the verge of being remade by yet another new technology: generative AI, and the US economy has demonstrated noteworthy resilience since the pandemic. The impacts of these factors are outside the control of the federal government.

Takeaways

- Historically, elections minimally impact the stock market.

- Investors should tune out the noise of election periods and stick to their long-term investment strategy.

- The S&P 500 is historically expensive, yet this overvaluation is mainly concentrated in the technology sector, where AI is such a factor. There is considerable cash on the sidelines which could provide a tailwind to risk assets as it is redeployed.

- With higher fixed income yields, remain invested in bonds through active bond managers who can manage toward more favorable bond sectors.

- We do not know the next catalyst which will trip up the stock market. With greater uncertainty and potential volatility, investors should be broadly diversified to allow for multiple outcomes.

If you have any questions or wish to review your portfolio asset allocations, please consult your JMG Advisor.

Important Disclosure

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by JMG Financial Group Ltd. (“JMG”), or any non-investment related content, made reference to directly or indirectly in this writing will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this writing serves as the receipt of, or as a substitute for, personalized investment advice from JMG. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. JMG is neither a law firm, nor a certified public accounting firm, and no portion of the content provided in this writing should be construed as legal or accounting advice. A copy of JMG’s current written disclosure Brochure discussing our advisory services and fees is available upon request. If you are a JMG client, please remember to contact JMG, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. JMG shall continue to rely on the accuracy of information that you have provided.

To the extent provided in this writing, historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices. Indices are not available for direct investment.

Market Segment (index representation) as follows: U.S. Large Cap (S&P Total Return); U.S. Mid-Cap (Russell Midcap Index Total Return); Foreign Developed (FTSE Developed Ex U.S. NR USD); Emerging Markets (FTSE Emerging NR USD); U.S. REITs (FTSE NAREIT Equity Total Return Index); Foreign REITs (FTSE EPRA/NAREIT Developed Real Estate Ex U.S. TR); U.S Bonds (Bloomberg US Aggregate Bond Index); U.S. TIPs (Bloomberg US Treasury Inflation-Linked Bond Index); Foreign Bond (USD Hedged) (Bloomberg Global Aggregate Ex US TR Hedged); Municipal Bonds (Bloomberg US Municipal Bond Index); High Yield Bonds (Bloomberg US Corporate High Yield Index).