Investing at Market Highs and Times of Uncertainty

INVESTMENT COMMITTEE COMMENTARY AUGUST 2021

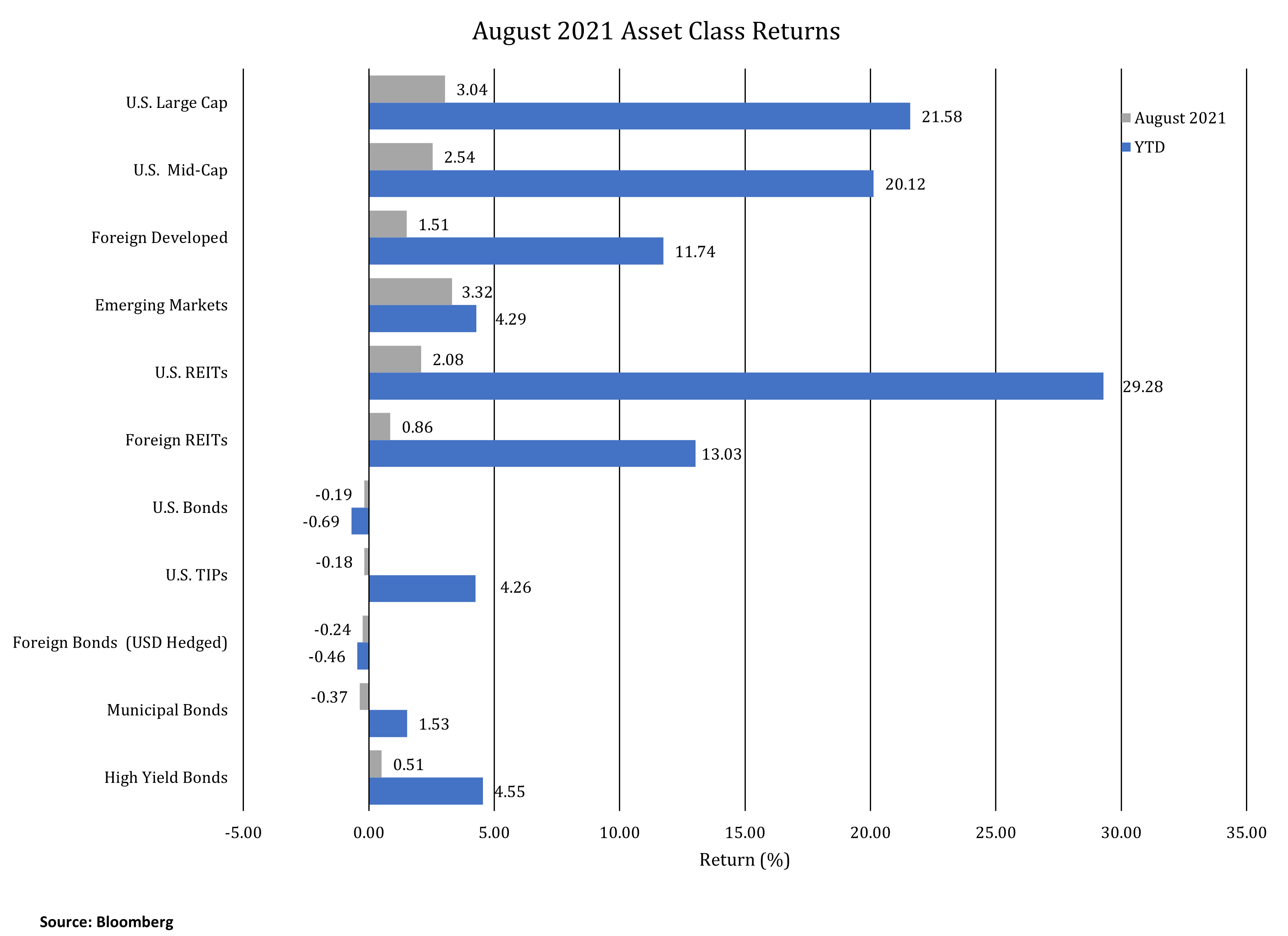

Asset class performance in August was mixed. Equities had positive performance, while fixed income had negative performance as interest rates increased during the month. After flat performance for most of the month, real estate investment trusts (REITs) moved positive in the last two trading days of August.

U.S. equities rose to new highs, in part, due to signals from Fed Chair Powell that while the central bank would begin tapering its monthly bond buying program, it would be in no hurry to raise short-term interest rates from near zero.

The yield on 10-year U.S. Treasuries rose from 1.24% to 1.30%. As a result, bond prices fell modestly in August. Year to date, while the return of the Bloomberg U.S. Aggregate Bond Index is -0.69%, U.S. Treasury Inflation Protected Securities (TIPS), municipal bonds and corporate high yield bonds are in positive territory.

Investing at Market Highs and Times of Uncertainty

We have had recent conversations with clients about whether putting new money to work in the midst of current market conditions is appropriate. The S&P 500 and Nasdaq are at or near all-time highs. Bond yields remain low and the Fed remains accommodative. Headline inflation has moved higher based on current prices compared to mid-pandemic prices one year ago. Tax increases are anticipated and geopolitical risks are elevated. Does it make sense to invest when stocks are at all-time highs and in a period when future stock and bond returns are expected to be low?

Experience has shown that it is difficult to identify a market high and attempts to do so are unreliable and often unprofitable. JP Morgan examined how investors have historically fared when investing at these market highs. They analyzed the performance of the S&P 500 from January 1988 through June 2021. Specifically, how did performance differ if one invested on any day versus investing only at all-time highs? The study compared subsequent 1, 3 and 5-year forward returns. Surprisingly, the forward cumulative returns were higher for investors investing at market highs (1-year: 12.2% vs. 15.0%, 3-year: 39.5% vs. 49.9%, and 5-year: 72.6% vs. 79.2%.).

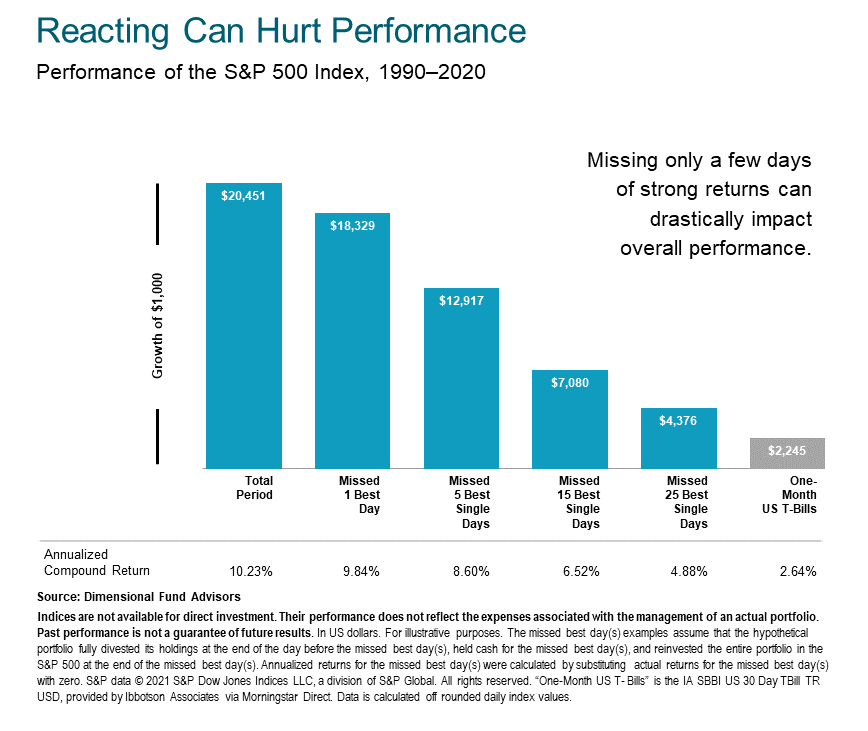

Momentum at market peaks appears to have overcome valuation concerns in the past. Staying invested remains an important discipline. Research demonstrates the impact from missing just a few strong days in the market. One study by Dimensional Advisors on the S&P 500 between 1990 and 2020 shows the performance effects of missing the top market days.

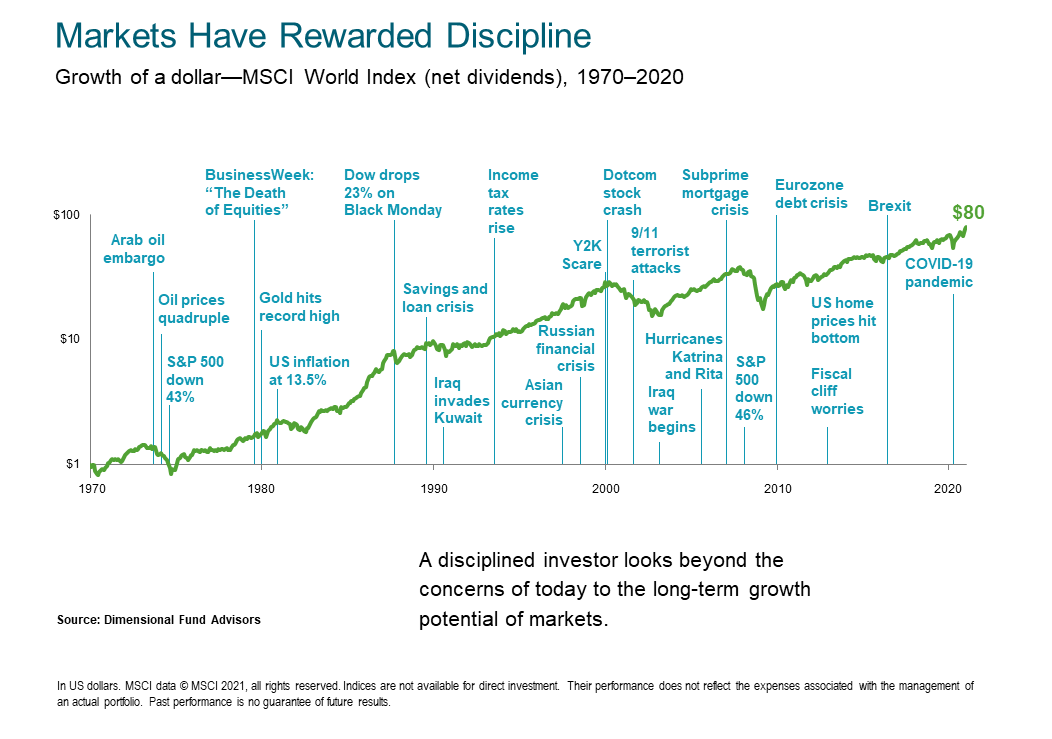

The good news is that investors do not need precise market timing to have a positive investment experience. The key is to remain disciplined and ignore short-term noise. By focusing on things that can be controlled such as asset allocation, diversification, fund expenses, turnover, and taxes, investors are able to earn the returns offered by the capital markets. The chart below shows that equity markets have performed well in the long-run despite numerous adverse events and short-term concerns.

We acknowledge today’s market environment seems extreme and in some ways we are in uncharted territory. However, uncertainty is always an element of investing. Associated risks need to be evaluated. We will always encourage and recommend investment discipline and exercise professional judgment when managing our clients’ investments through whatever market environment is presented.

If you have any questions, you should consult with your JMG Advisor.

Important Disclosure

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this writing, will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this writing serves as the receipt of, or as a substitute for, personalized investment advice from JMG Financial Group, Ltd. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. JMG is neither a law firm nor a certified public accounting firm and no portion of the content provided in this writing should be construed as legal or accounting advice. A copy of JMG’s current written disclosure statement discussing advisory services and fees is available for review upon request.

To the extent provided in this writing, historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices. Indices are not available for direct investment. Market Segment (index representation) as follows: U.S. Large Cap (S&P 500 Total Return); U.S. Mid-Cap (Russell Midcap Index Total Return); Foreign Developed (FTSE Developed Ex U.S. NR USD); Emerging Markets (FTSE Emerging NR USD); U.S. REITs (FTSE NAREIT Equity Total Return Index); Foreign REITs (FTSE EPRA/NAREIT Developed Real Estate Ex U.S. TR); U.S. Bonds (Bloomberg US Aggregate Index); U.S. TIPs (Bloomberg US Treasury Inflation-Linked Bond Index); Foreign Bonds (USD Hedged) (Bloomberg Global Aggregate Ex US TR Hedged); Municipal Bonds (Bloomberg US Municipal Bond Index); High Yield Bonds (Bloomberg US Corporate High Yield Index).