2024 in Review

INVESTMENT COMMITTEE COMMENTARY December 2024

Stocks trended lower in December as the S&P 500 retreated from all-time highs. Investor optimism declined following the Federal Reserve’s (Fed’s) December meeting. As expected, Fed Chair Jerome Powell announced a cut in the fed funds interest rate by 0.25%. However, Powell’s commentary on future rate cuts had a more tempered tone. The Fed expects only two rate cuts in 2025, less than what investors were expecting. The Fed’s decision was based on its higher projection for gross domestic product (GDP) of 2.5% coupled with a lingering U.S. unemployment rate near 4% and inflation estimates above the Fed’s 2% target rate. Powell noted that “our policy stance is less restrictive, and … we can therefore be more cautious as we consider further adjustments to our policy rate”. Effectively, with the U.S. economy remaining resilient and not showing imminent signs of recession, further rate declines do not have to be hurried.

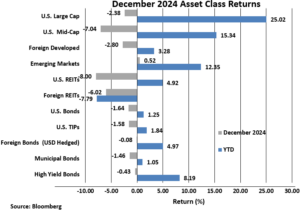

The S&P 500 fell 2.4% in December, but finished strong for the year, up 25.0%. The broader equity asset classes had steeper declines for the month as U.S. mid-cap stocks and real estate investment trusts (REITs) fell 7.0% and 8.0%, respectively, but finished higher for the year. Foreign developed country equities fell 2.8% but emerging market equities had a nominal gain of 0.5%. While foreign and emerging market stock performance for the year was positive, the weaker currencies relative to the U.S. dollar detracted from those returns.

Bonds also had weak December performance giving back much of the gains they had shown earlier in the year. With the Fed announcement and following the November presidential election, the yield on 10-year Treasury bonds moved higher from 4.18% to 4.58% and the U.S. dollar rose to its highest level since 2022. The Fed is currently less accommodative than foreign central banks based on the strength of the U.S. economy. The Bloomberg U.S. Aggregate Bond Index (AGG) fell by 1.6% for the month. Other bond sub-indexes also declined in December.

2024 in Review

2024 was strong for the U.S. economy and the financial markets. High interest rates, rising unemployment, turmoil in the Middle East, and the ongoing Russia/Ukraine war, were some of the factors that could have signaled economic contraction and a downturn in the stock market. Yet, the opposite occurred. Gross domestic product expanded by 3.1% in the third quarter and 2.9% year over year. Major stock market indexes posted solid calendar year gains. Headline inflation fell while S&P 500 corporate earnings grew by 8.7% and recent profit margins impressively grew by 12.8% (3Q24).

Shifts in investor sentiment contributed to increased market volatility in 2024 based on inflation data points, recession concerns, expectations of Fed rate cuts and potential tax and tariff policy changes. The following chart shows the monthly total returns of the S&P 500 and illustrates sentiment inflection points throughout 2024.

The following highlights selected key issues and events experienced by the markets in 2024:

- S&P 500 / The “Magnificent 7” – Continuing a trend from 2023, only a small number of large cap U.S. stocks were responsible for the outperformance of the S&P 500 in 2024. Magnificent 7 stocks (Apple, Amazon, Google, Meta, Microsoft, Nvidia and Tesla) had a total return of approximately 48% in 2024, compared with 25% for the S&P 500. The S&P 500 excluding the Magnificent 7 stocks earned approximately 10% in 2024 (Source: JP Morgan Asset Management). Because of the large disparity in performance by the largest S&P 500 companies, the forward price / earnings ratio of the largest companies is approximately 30x, a very high multiple. With the continued outperformance of the Magnificent 7, concentration risk in the S&P 500 is becoming a concern. The top 10 stocks in the index (which includes the Mag 7) now represent almost 39% of the index and is more than double the concentration 10 years ago.

- Inflation – In 2024, the consumer price index (CPI) declined intermittently, but consumers faced the stark reality of a high overall cost of living. Prices for food rose 2.4% for the 12 months ending in November, while shelter prices rose 4.7%. CPI moved from 3.1% in January to a low of 2.4% in September before ticking higher to 2.7% in November. The level of inflation remains above the Fed’s 2.0% target. With progress in moderating price pressures, coupled with economic resilience, the Fed cut interest rates by 100 basis points (1%) in 2024 to the current range of 4.25%-4.50%.

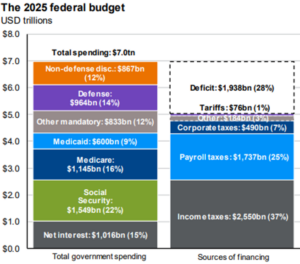

- Federal Deficit – For fiscal year 2024, which ended September 2024, the government deficit was $1.8 trillion. Congress will be challenged in dealing with this deficit as about 88% of the federal budget is comprised of “mandatory spending” (Social Security, Medicare, Medicaid, and Defense). With tax revenues only projected to cover 72% of spending, balancing the budget will require some combination of cutting mandatory spending and raising tax revenues. If Congress does not take fiscal policy action, the current level of deficits and U.S. debt is not sustainable and could be a headwind to stock performance.

- Recession – A recession in 2024 did not occur as many people expected. At the end of 2024, the Treasury yield curve is mostly in a normal configuration and only inverted at the short end of the curve. This condition improved in 2024 and gives more hope of a “soft landing” where the U.S. economy avoids recession. Recession risk has not been completely eliminated but this risk appears to be less than a year ago.

- International Markets – The strength of the U.S. dollar significantly offset strong returns in non-U.S. stocks in 2024 for U.S. dollar-based investors. In local currency, the MSCI All Country World ex-U.S. index had a return of 13.2% but after the currency effect, the return to U.S. investors was 6.1%. If the U.S. dollar were to weaken, the currency effect will have the opposite effect for U.S. investors with more favorable foreign stock returns.

2025 Views and Commentary

Markets begin 2025 with great expectations in anticipation of tax cuts and pro-business deregulation from the Trump administration and the continued impact of artificial intelligence (AI) across the economy. Stocks could be propelled higher through a continued economic soft landing coupled with further Fed rate cuts. However, because of high stock valuations and many economic and geopolitical uncertainties, market risks remain significant in 2025.

Key factors to watch in 2025 are the same factors that have created the “Goldilocks Effect” of the past two years.

Corporate Earnings: Market valuations are high for the S&P 500, especially for the large Magnificent 7 and AI related companies. Earnings growth in those companies must continue to outpace expectations for these lofty valuations to be justified. Consensus 2025 earnings per share (EPS) growth for the S&P 500 is close to 15% and approximately double the historical average. Earnings season must continue to report strong results and strong forward-looking commentary. If earnings guidance disappoints, market multiples may fall.

Pro-Growth Policies: Investors are eagerly awaiting the implementation of pro-growth policies from the Republican Congress and Trump administration. If executed, the extension of the 2017 Tax Cuts and Jobs Act and possible additional corporate and personal tax cuts, and sweeping deregulation could result in increased corporate earnings, increased personal income and increased consumer spending (all of which are positive for stocks). A failure to follow through on these expectations is a downside risk, while overly stimulative policies may drive inflation and interest rates higher.

Geopolitical Tensions: While these remained high in 2024, investors finished the year with hopes for progress on ceasefire agreements in the Middle East and Eastern Europe. A sharp increase in global political tensions, particularly to the degree it disrupts trade, could be seen as a negative for global growth and thereby equity markets.

Monetary Policy: Investors are familiar with the Fed’s dual mandate: maximum employment and price stability. Equity investors hope for lower interest rates to promote economic growth. But if Fed expectations are not met, and interest rates stall or rise, stock market volatility could increase. This can be seen in the monthly returns of the S&P 500 referenced previously.

Inflation: CPI seems to be settling at a higher level than the 2% Fed target. Further, the new administration’s pro-business, pro-growth economic proposals have the potential to be inflationary. Higher inflation would likely reduce Fed rate cut expectations and send interest rates higher, which could be negative for markets.

Unemployment: If the U.S. unemployment rate remains in the low 4% range, this would be in line with market expectations. A stronger than expected jobs report could reduce Fed rate cut expectations, while a weak jobs report may indicate a slowing economy – either of which could be negative for equity markets.

Conclusion

Current conditions appear more optimistic but also riskier than a year ago. The current relatively high valuation of the S&P 500 is based on optimism around AI and the incoming administration’s pro-growth policies. Disappointment on any number of fronts could trigger a change in confidence and in turn a downturn in markets. We caution about having too much portfolio concentration risk in the largest S&P 500 companies. Market volatility will more likely be higher than the lower levels experienced in much of 2024.

Diversification through smaller and midsize US companies as well as non-US stocks where valuations are currently lower is always an important tool to manage investment risks.

We believe that client investment portfolios are well-positioned for a myriad of potential outcomes.

A Final Note on Cybersecurity

At JMG, we have policies, procedures, conduct ongoing training for our staff and utilize security technology to ensure we protect your data. It is also essentially important for you, our clients, to be vigilant in protecting your own personal information. Fraudsters have become much more sophisticated in their methods for obtaining personal information using phone, email, and text messages. We are aware that brokerage account holders with major custodians like Schwab are being targeted in an increased fashion. For this reason, we want to remind all our clients to be cautious, be aware and understand the techniques being used by fraudsters.

The Schwab website provides a lot of good information on keeping your accounts secure at https://www.schwab.com/schwabsafe.

If you have any questions, please consult your JMG Advisor.

Important Disclosure

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by JMG Financial Group Ltd. (“JMG”), or any non-investment related content, made reference to directly or indirectly in this writing will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this writing serves as the receipt of, or as a substitute for, personalized investment advice from JMG. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. JMG is neither a law firm, nor a certified public accounting firm, and no portion of the content provided in this writing should be construed as legal or accounting advice. A copy of JMG’s current written disclosure Brochure discussing our advisory services and fees is available upon request. If you are a JMG client, please remember to contact JMG, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. JMG shall continue to rely on the accuracy of information that you have provided.

To the extent provided in this writing, historical performance results for investment indices and/or categories have been provided for general comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your account holdings correspond directly to any comparative indices. Indices are not available for direct investment.

Market Segment (index representation) as follows: U.S. Large Cap (S&P Total Return); U.S. Mid-Cap (Russell Midcap Index Total Return); Foreign Developed (FTSE Developed Ex U.S. NR USD); Emerging Markets (FTSE Emerging NR USD); U.S. REITs (FTSE NAREIT Equity Total Return Index); Foreign REITs (FTSE EPRA/NAREIT Developed Real Estate Ex U.S. TR); U.S Bonds (Bloomberg US Aggregate Bond Index); U.S. TIPs (Bloomberg US Treasury Inflation-Linked Bond Index); Foreign Bond (USD Hedged) (Bloomberg Global Aggregate Ex US TR Hedged); Municipal Bonds (Bloomberg US Municipal Bond Index); High Yield Bonds (Bloomberg US Corporate High Yield Index).